A lifetime mortgage and a home reversion plan are the two main forms of equity release in the UK, and they differ fundamentally in how they generate cost over time. A lifetime mortgage builds debt through compound interest, while home reversion transfers a share of future property value at a discount. The cheaper option depends on lifespan, house price growth, and inheritance goals.

In this guide, we’ll break down how each works and which typically costs less in the long run.

TL;DR:

-

- A lifetime mortgage builds debt through compound interest while the borrower keeps full ownership

- A home reversion plan sells a share of the property at a discount, reducing future value permanently

- Lifetime mortgages often cost less long term, especially with rising house prices and shorter occupancy

- KIS Finance’s calculator helps estimate equity release interest rates and total cost before choosing

What is a lifetime mortgage?

A lifetime mortgage is a loan secured against your property that allows homeowners aged 55 or older to release tax-free cash without selling their home. The borrower retains full ownership, and the loan plus rolled-up interest repays when the property sells after death or entry into long-term care. Interest compounds over time, which increases the total amount owed.

Most plans follow Equity Release Council standards, including a no negative equity guarantee and the right to remain in the home. Tools such as KIS Finance provide a Lifetime Mortgage Calculator that models equity release interest rates and long-term costs.

What is a home reversion plan?

A home reversion plan is an equity release product where a homeowner sells part or all of their property to a provider in exchange for a lump sum or regular payments. The homeowner keeps the legal right to live in the property, usually rent-free, for life.

The provider buys the share below market value, which creates the long-term cost. Unlike lifetime mortgages, no interest accumulates, but the provider owns a fixed percentage of the future sale value.

Here’re the key features of a home reversion plan:

- Sale of 25%–100% of the property at a discounted price

- No interest or loan repayment during the homeowner’s lifetime

- Fixed share of ownership transferred to the provider from the start

- Full exposure of the sold share to future house price growth

- Regulated plans often follow Equity Release Council standards

This structure creates a clear contrast in any lifetime mortgages comparison, as the cost comes from surrendered equity rather than interest accumulation.

Lifetime mortgage vs home reversion: Which is cheaper in the long run?

A lifetime mortgage usually costs less over time when house prices rise and the borrower does not stay in the property for several decades. A home reversion plan sets a fixed loss from the start, which can become expensive if property values increase.

The outcome depends on lifespan, interest rates, and market growth.

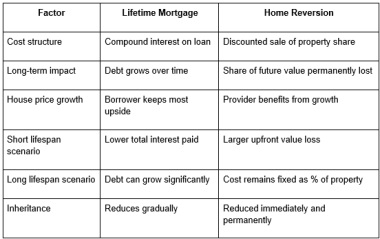

Let’s compare:

Overall, a lifetime mortgage often remains the cheaper route, but long occupancy and high interest rates can narrow the gap.

Conclusion

A lifetime mortgage and a home reversion plan solve the same need but produce very different long-term outcomes.

A lifetime mortgage often results in lower total cost when the borrower does not remain in the property for decades and when house prices increase, while a home reversion plan offers certainty, as the percentage sold stays fixed from the start.

The choice depends on personal circumstances:

- Choose a lifetime mortgage for flexibility, higher cash release, and exposure to future property value

- Consider home reversion for predictable outcomes and no interest accumulation

- Review Equity Release Council safeguards before committing

- Compare projections over 10–30 years to assess total cost and inheritance impact

A clear comparison based on lifespan and property growth gives the most reliable answer.

FAQs

What is the main difference between a lifetime mortgage and a home reversion plan?

A lifetime mortgage is a loan secured against a property where interest compounds and repays later from the sale. A home reversion plan involves selling a share of the property at a discount while retaining the right to live there. Ownership stays with the borrower in a lifetime mortgage but transfers partially or fully in home reversion. The cost arises from interest in one and lost equity in the other.

Which option is cheaper in the long run?

A lifetime mortgage usually results in lower long-term cost when house prices grow and the borrower does not remain in the property for 20–30 years. Home reversion can become expensive because the provider owns a fixed share that benefits from full market appreciation. Long lifespan and high equity release interest rates can reduce the cost advantage of a lifetime mortgage. The outcome depends on property growth, age, and duration.

When does a home reversion plan make more sense?

A home reversion plan suits borrowers who want certainty and no exposure to interest accumulation. It works well for those planning long-term occupancy and who accept a reduced estate from the start. Stable or declining property markets can also make reversion relatively more predictable. The trade-off remains the permanent loss of a share of future property value.